A Primer on FSCO Auto Insurance Rate Approvals

On April 13, Ontario’s auto insurance regulator, the Financial Services Commission of Ontario, FSCO, posted an auto insurance rate increase on average of 2.23 per cent for the first quarter of 2018. This isn’t the first rate increase we have seen lately. In fact, FSCO has approved rate increases 6 of the last 8 quarters totalling an overall increase of 6.85 per cent!

These increases show just how confident insurance companies are that consumers are getting used to ever-increasing insurance rates for ever-decreasing coverage. The determination to seek increases and squeeze more out of Ontario’s beleaguered motorists and injured accident victims was telegraphed by many insurance companies over the last few months as they reported their year-end results.

A disproportionate focus on claims costs – and nothing said about profits!

This rate increase was significant news with a little more than 7 weeks before the election in which at least part of the focus will be on auto insurance. You should take a good look at the breakdown of auto insurance claims costs provided with this quarterly bulletin.

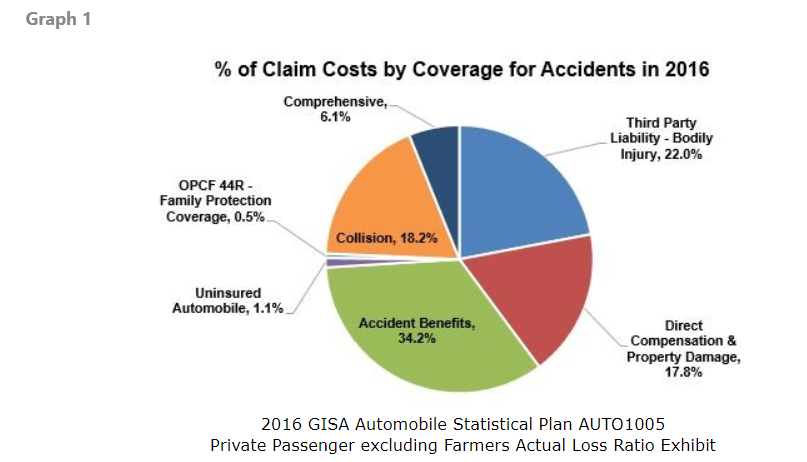

Here is the pie chart from the FSCO website showing the relative percentage of claims in Ontario, based on data provided by the General Insurance Statistical Agency (GISA), loss ratio exhibits.

While this information seems straightforward enough, there are problems with it.

The first issue concerns a lack of transparency and accountability. Why is that? The reason is that the claims breakdown does not tell the entire story.

Your auto insurance premiums pay for hefty insurance industry administration costs and profits in addition to all the claims payouts in any given year. The omission of that information leaves the unmistakable conclusion that claims are the only significant cost in the auto insurance business.

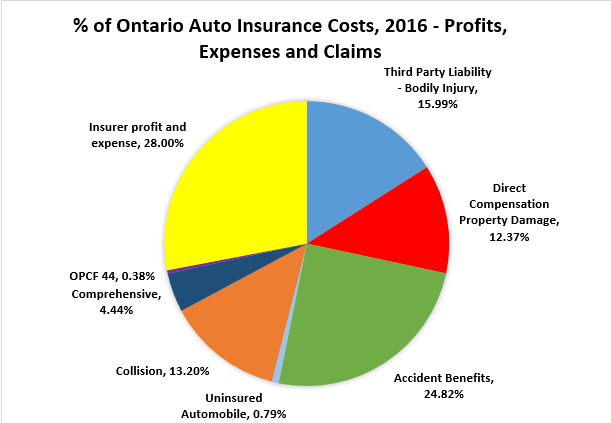

The insurance industry is really good at reminding us that rising claims costs, not to mention pervasive fraud, are both significant problems. We do not need the regulator playing into and supporting that narrative by presenting incomplete information that actually exaggerates the true extent of claims costs at the same time that same regulator is announcing the approval of rate increases. When you factor in both profit and administration costs, which happen to be the biggest piece of the pie, the relative size of claims decline, as the pie chart below shows.

The public would be better served if the provincial regulator provided a more complete picture. What is clearly needed is a more transparent and comprehensive breakdown of all costs and not just the selected information that is currently provided. We need that kind of transparency when it comes to auto insurance, which is unique as a compulsory financial service. Why should we accept less?

A pattern of misleading data

This is not the first time that FSCO has published misleading data on the insurance industry. One only has to refer back to the Three-Year Review Report released in 2014 to find data on Bodily Injury claims that was highly suspect. It is deeply problematic that this data – which was proven to be wildly inaccurate by subsequent GISA reports for bodily injury – was quoted without any corrections made and used to support and drive policy decisions, as was seen in the Marshall Report released a year ago.

We need greater transparency and clarity in insurance claims and financial data. Let’s move to a more complete data picture in the future with better disclosure for consumers.